Credit: Envato

Credit: EnvatoSVB Collapse: Real Estate Turmoil Begins in Europe?

See the thoughts of real estate leaders and economists on the current banking event and whether a financial crisis is looming

GRI’s online meeting, SVB Collapse & Beginning of Banking Turmoil, took place on the 23rd of March for approximately 150 international leaders of real estate to discuss the impacts on real estate and possible systemic challenges of recent events.

Claus Vistesen, the Chief Eurozone Economist at Pantheon Macroeconomics, spoke on the future of the global economy, while our very own CEO, Gustavo Favaron, moderated the discussion.

Other co-chairs of the event included:

-

Cristina García-Peri, Managing Partner/Director of Strategy and Corporate Development, Grupo Azora;

-

Kathryn Ogden, Global Head, Real Estate Corporate Banking and Real Estate Capital Partners, RBC Capital Markets;

-

Michael Covarrubias, Chairman & CEO, TMG Partners.

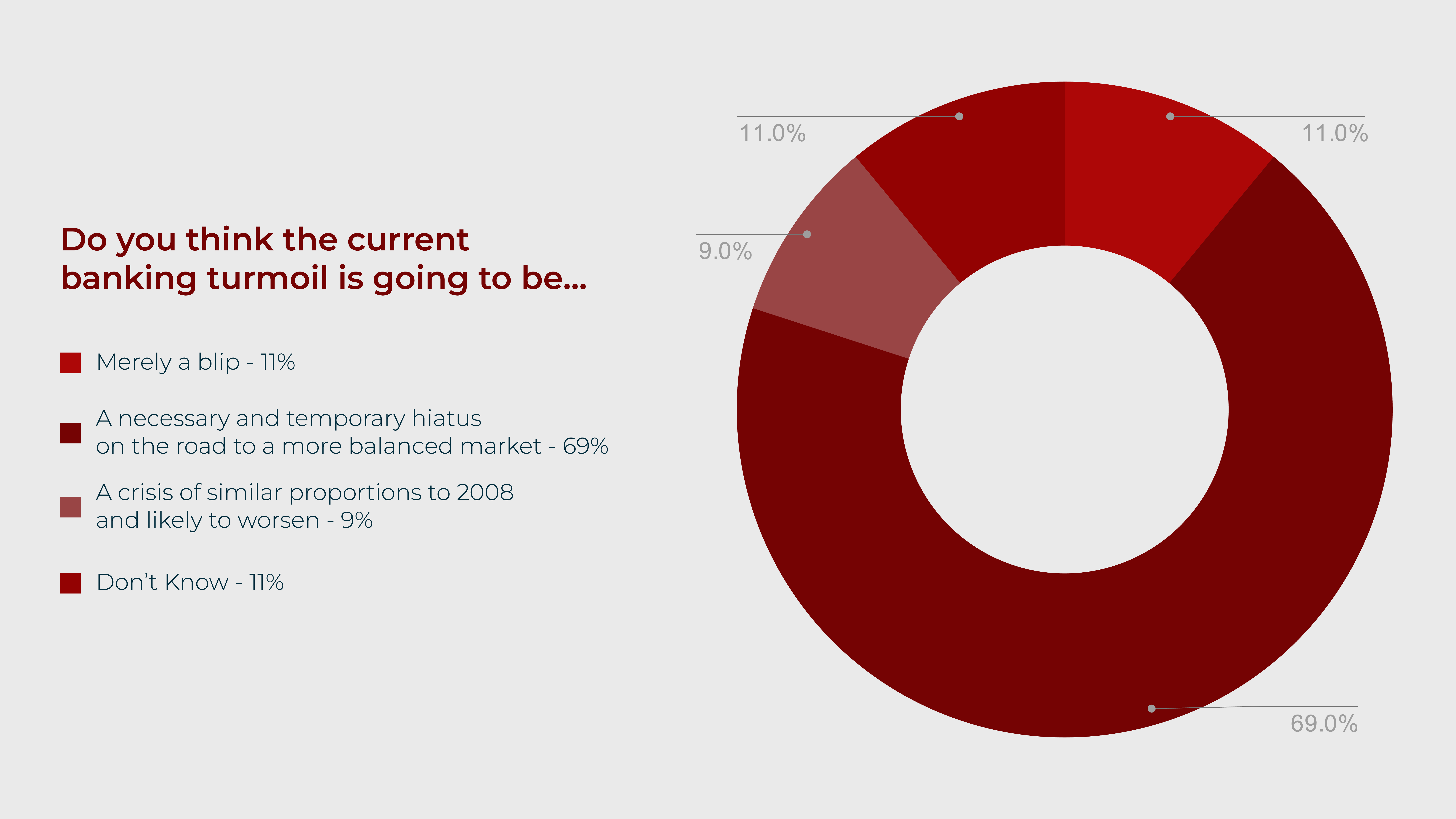

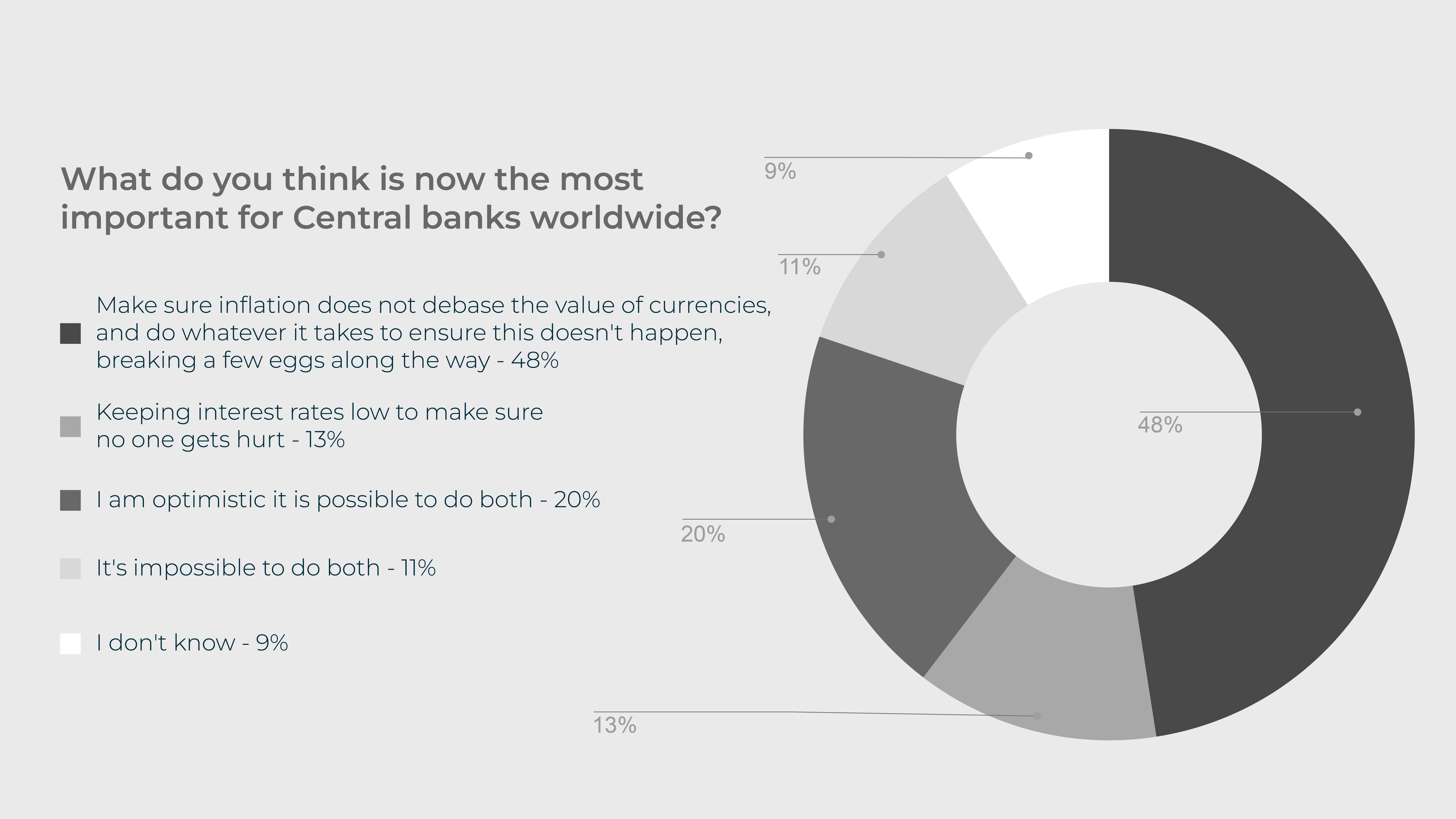

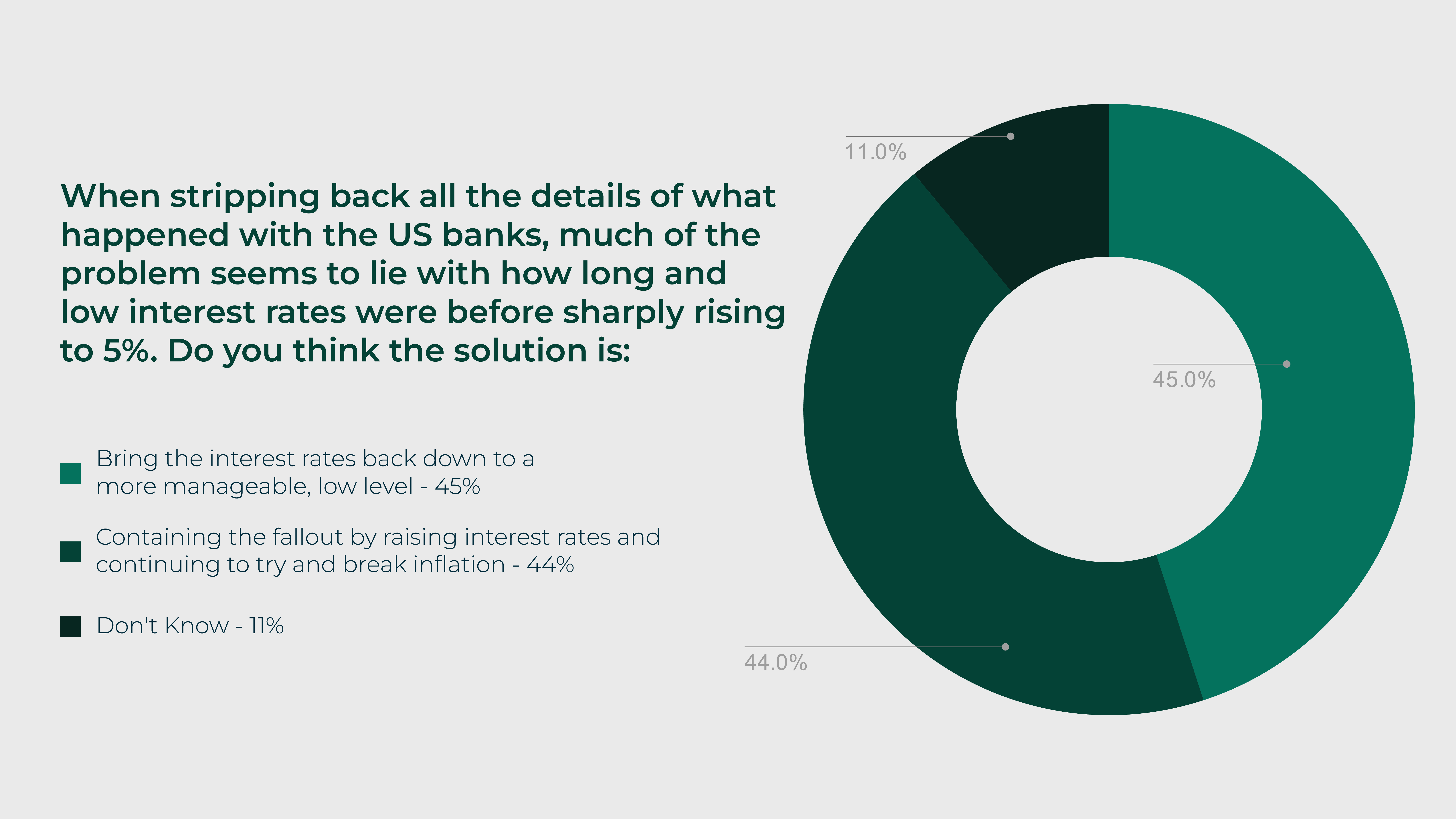

The consensus at the meeting was that this event is not the beginning of a new global financial crisis with only 9% stating that this is a crisis of similar proportion to 2008 that’s likely to worsen. Rather, the majority, 69%, thought that this is a necessary and temporary hiatus on the road to a more balanced market.

There are two reasons why this is not the case: the first is macroeconomics, as a financial crisis happens when there are big imbalances in the economy, and the current environment does not have these imbalances to a great extent. Although the economy is always vulnerable to financial stability risks, there is not a great amount of instability this year.

Additionally, the US is diversified and does not rely completely on banks for financing, which means that there is less concern about the economy collapsing entirely. Europe is bank-based and finances itself via banks, so could face more distress if put in this situation directly.

The second reason is that the political landscape has changed significantly in the past 15 years. Politicians are less prone to deliberating and more likely to make immediate decisions to solve emerging issues; see the UK’s quick decision to endorse HSBC’s purchase of SVB UK in recent weeks. This way, the few are sacrificed to protect the many, as although it is possible Credit Suisse or Silicon Valley Bank could have survived on their own, authorities would rather make interventionist decisions at their expense to ‘save’ the rest of the economy.

What does the SVB collapse mean for real estate?

There is less good news for the real estate industry, as the heads of real estate attending the online meeting agreed that this event will tighten financial and credit conditions for those operating in this space. There will be a lack of available credit as banks become more conservative and begin to make even more conservative decisions than before.

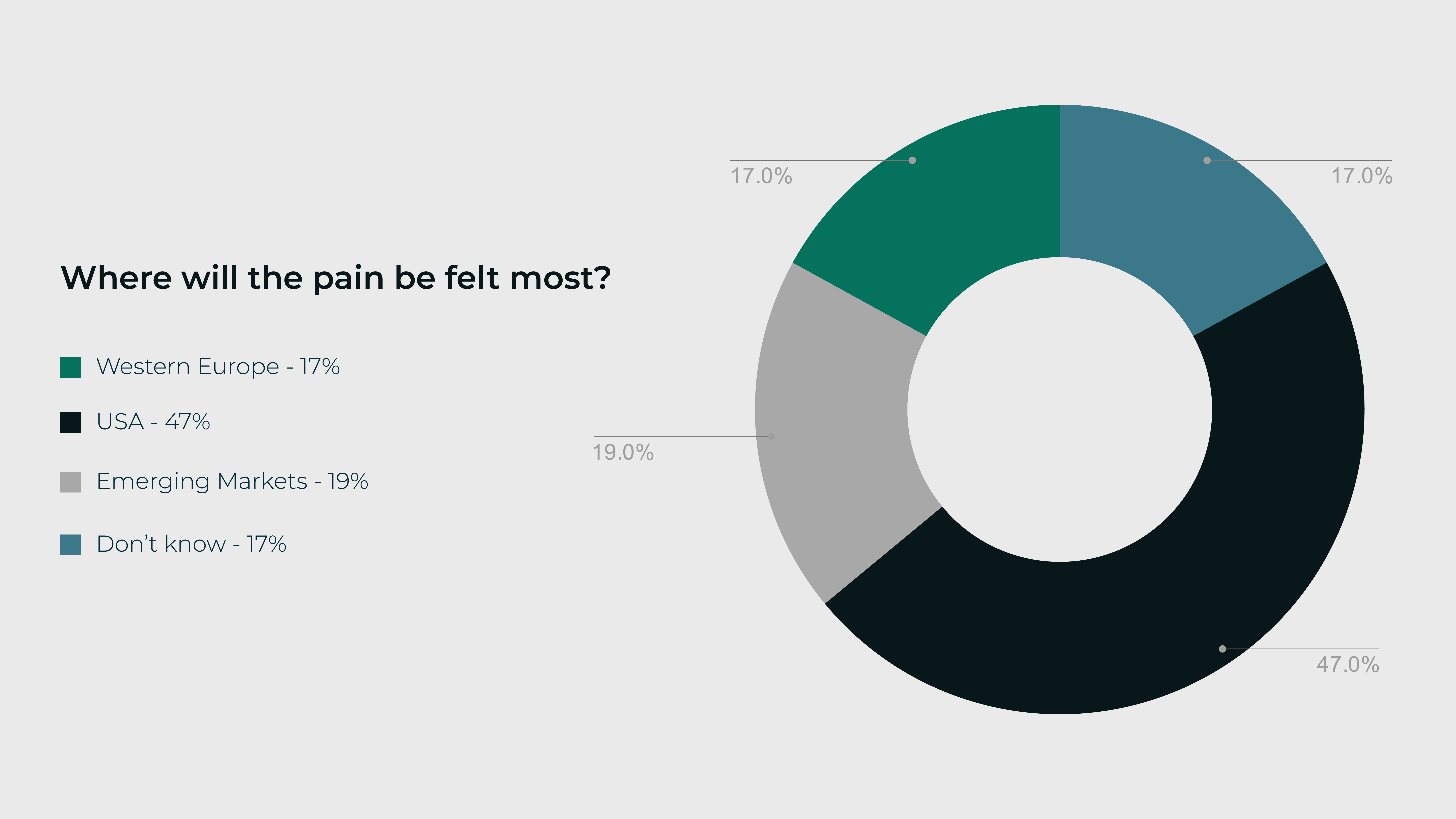

This financial tightening will occur mostly in the USA, where regional banks have been lending on smaller deals, but are more active than major banks in the real estate space.Thus there will be enhanced caution from smaller banks, as there will be an increase in the cost of funds for self-funding for banks themselves.

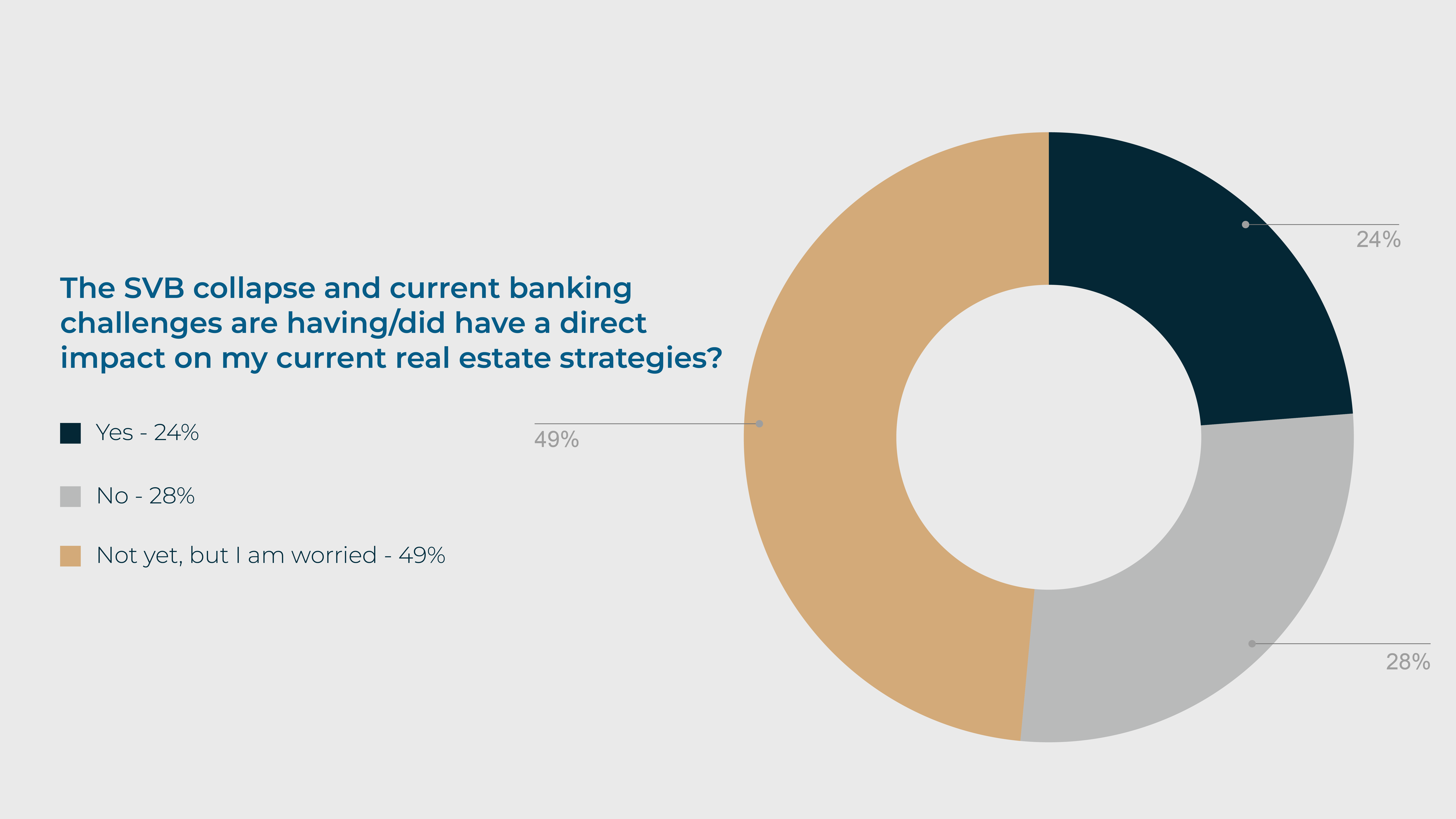

Those who answered yes in the survey:

The European attendees who imagine that there will be repercussions on real estate say that there will be an impact due to lack of credit specifically from the USA, which is one of the biggest investors in Europe, and also opens up opportunities for other areas such as Asia and the Middle East to replace the US.

- Europe will see repercussions as it has demonstrated a huge amount of focus on bank capital, and confidence is very important in this scenario.

- Smaller banks have suffered from nervousness, and it is important to note that there is no single example of such a peculiar situation as the one we are currently in.

- There are some jurisdictions where real estate companies have been leveraging very highly, such as Germany and Sweden, taking advantage of low-interest rates, and this may cause difficulty.

- The ECB is focused on the commercial exposure of European banks, making banks more conservative.

High-leverage products will have difficulty refinancing and should expect expensive alternative lenders to be some of the only options in the coming months. Meanwhile, low-leverage operating assets with good tenants will still find financing.

Offices at the forefront

Across the board, Offices were already hit by the WFH movement and credit standards were tightening. Offices have long-term leases, so they skated by during the pandemic, and now problems are emerging.

In the US, Offices will certainly be affected the most by this incident. However, Offices beget Residential, which begets Retail; ultimately, they are all connected, just as interest rates have an impact on all assets. Some at the meeting asserted that there will be no loans on Offices whatsoever as real estate moves from an active market with capital fluidity to no debt available. The deals available will ask for huge down payments.

“Public markets are the canary in the coal mine.”

- Real estate leader at SVB Collapse

In the UK, Offices were already seeing a difficult period with only equity available to finance projects. At this time, developers are even less inclined to look at locations even slightly out of the main cities as cap rates have skyrocketed. Companies currently holding assets with debt need to generate liquidity and capital, but it is difficult to refinance. Cash buyers and private investors will buy, but leverage is ‘out of the game’, and selling these assets at the moment will be challenging.

Offices are seeing ‘carnage’ in the public sector due to a perceived fall in demand; most know that Offices won't be the same as pre-pandemic, so they don’t know why they would stay in those locations. There is no exit in some of these situations due to general increasing costs, as well as the cost of financing.

Short-term developments in real estate post-SVB crash

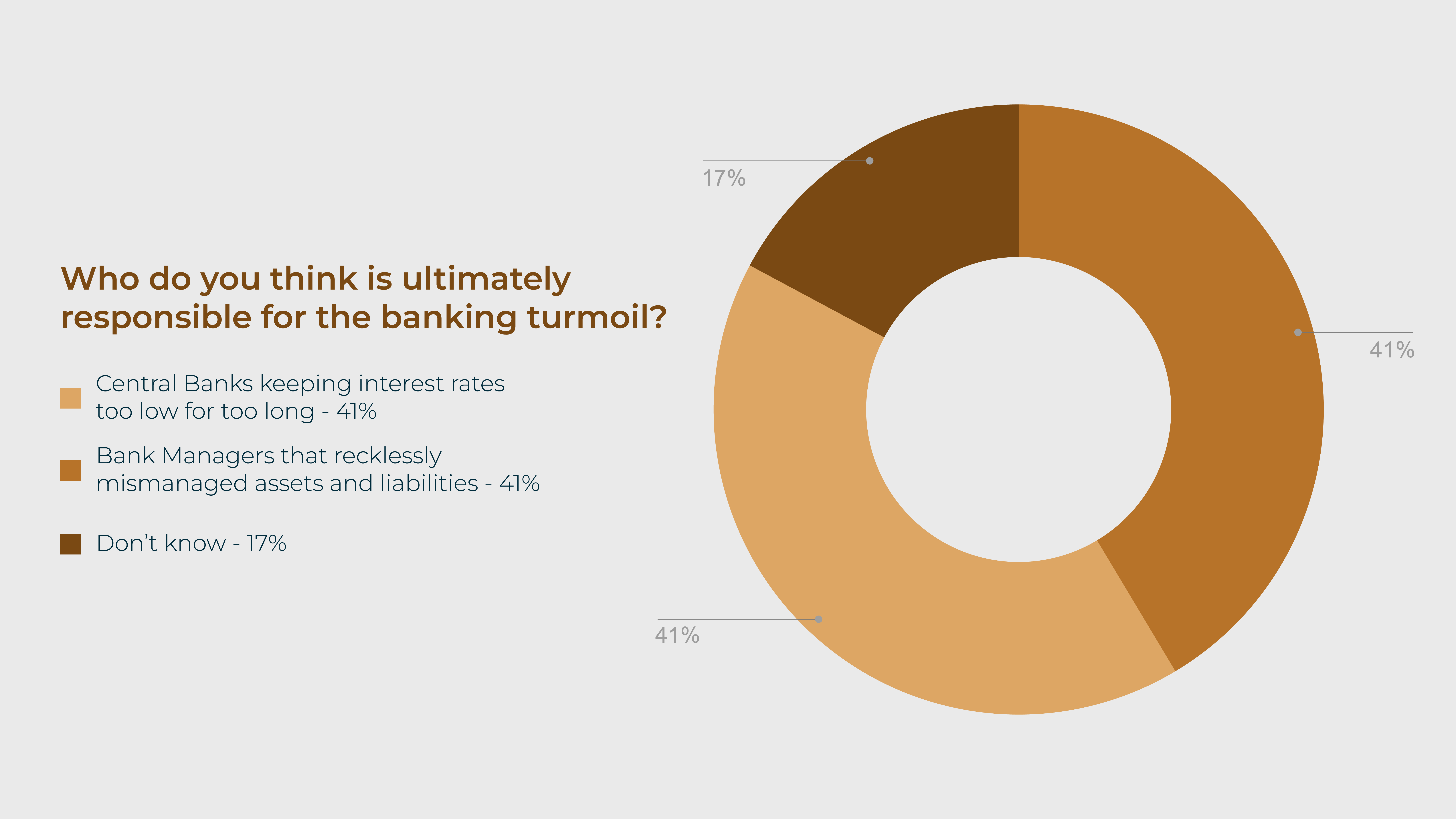

Ultimately, stress on banks is inevitable as rates were so low for so long, and have not only increased but have done so faster than expected. Real estate is a yield instrument and will be one of the first to see stress because of this. If interest rates were still 25 basis points, this wouldn't have happened so quickly.

The market has been affected differently than has been seen in the past, and attendees note that they have never before seen a recession where different sectors are still doing well while others suffer. Different markets are having very different results, for example in Texas, where cities such as Austin have not seen a credit squeeze.

Some also note that Europe still needs to see repricing for the majority of properties, as many owners have not come to terms and will not put in additional equity. High interest rates are here to stay, so prices need to be adjusted. One example of an asset class that has been adjusted is Logistics in the UK. After repricing, more capital may start to flow again.

It has already been predicted by central banks that interest rates will see a slowdown in the medium term, but will still be higher than before when they were almost too low. After all, interest is still negative in real terms due to inflation and many economies are still strong and real estate cash flows are good in Europe. Additionally, attendees assert that credit must be tightened in order to make inflation taper.

Some in the meeting even argued that underlying economic strength keeps driving inflation and interest higher, which continues to reduce the amount of capital available in the world. The cost of capital stress makes this situation different from a traditional recession. If the industry self-regulates by shutting down supply, you would expect some prices would stabilize, and buying will be initiated. At this time, private equity and alternative lenders will take advantage.

One important attendee question was: What is a healthy level of inflation?

- Experts say that below 5% is okay for real estate;

- Anything above that and asset market valuations get depressed;

- As part of the institutional framework, banks panic when they see inflation, as it is their job to control it;

- It may look bleak as, despite the turmoil, the bias of interest rates is still going to go up.

Main conclusions from the event

The current real estate landscape is one of recapitalisations and refiguring borrower-lender dynamics. Those operating in this space understand that there will be a change in deal flow and capital flow in the coming months as banks become more conservative. Meanwhile, alternative lenders will become more prominent in the market to fill the gap.

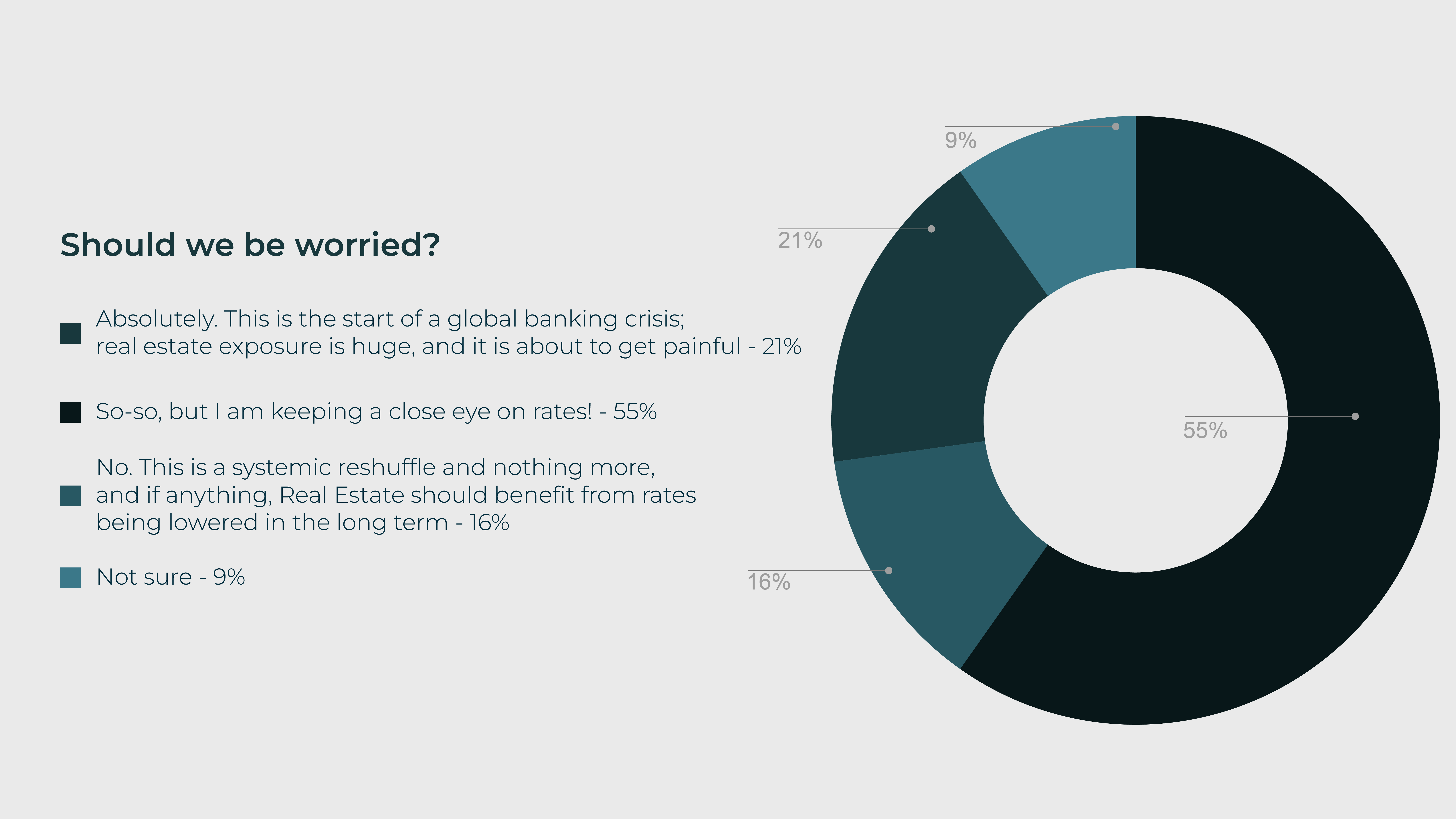

Still, only 21% of the GRI event attendees think that this is the start of a global banking crisis. The majority are rather more unsure, saying that they will be keeping an eye on interest rates.

For many of the attendees of last year’s Europe GRI, this crisis would not have come as much of a surprise. Europe GRI 2022 was for many the ‘calm before the storm’, and it was understood that there could be a recession or an occurrence possibly similar to the 2008 financial crisis.

For an opportunity to discuss macroeconomics, the trajectory of real estate and how to navigate the current challenges in the market, attend GRI’s flagship event, Europe GRI 2023 in September.

Written by Sarah Garnett