No attribution required

No attribution requiredInvestors expect 2020 to see the resurgence of UK retail

Demographic trends, investor interest and improving yields may be indicating an impending resurgence of the UK retail sector.

March 4, 2020Real Estate

The last few years have certainly proved to be a turbulent time for the UK’s real estate industry, with consistent news of store closures, administrations, and NPAs casting a dark cloud over the country’s shopping capitals. Some of the numbers even mirror the Global Financial Crisis, with year-on-year shopping centre rents dropping 5.1% in Q3 2019; the biggest drop since Q4 2009.

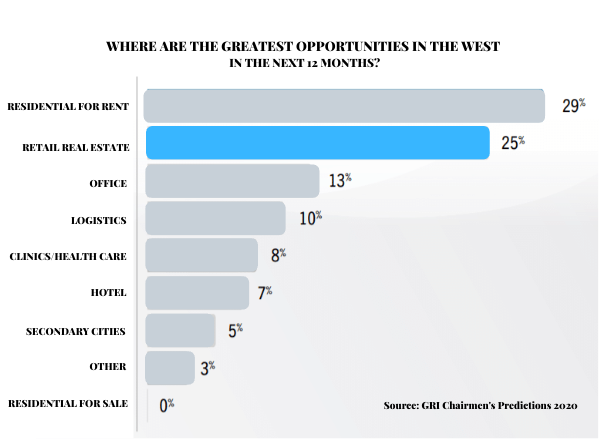

However, the key drivers shaping retail supply and demand are very different to that seen during the Financial Crisis, with such things as ecommerce and click and collect impacting the industry in ways that weren’t even comprehendable 10 years ago. This unchartered territory has unearthed some quite exciting opportunities: some of the largest transactions across Europe in the last 6 months have seen high-profile acquisitions of non-performing retail parks and shopping centres by companies ready to push them into the 21st century with updated technological and social strategies. With this, and global real estate leaders choosing retail as the second most promising asset in the next 12 months in the latest GRI Chairmen’s Predictions survey, 2020 might actually be the year that the UK and even Europe sees the resurgence of retail.

Investment in UK high street retail shops was fairly strong in 2019. One advisor told the GRI Hub that they estimated around £2bn of retail transactions took place in Q3 2019, compared to £1.8bn for the same period the previous year. Recent reports of large deals being made in London's prime retail locations may be indicative of a rising private investor interest in high streets.

The lack of interest in the shopping centres however has stunted growth, with a lacklustre Q3 2019 only clocking around £650mn in shopping centre deals (Preqin), compared to £974mn in the same period in 2018. However, this is despite super-prime shopping centres yielding 5.5% - the highest it's been since 2017 (Savills). Secondary and Tertiary yields were performing well too (11.25% and 14.5% yield respectively). The Q3 numbers also don’t reflect the growing interest in niche shopping centre assets, such as food anchored real estate.

But what investors are really looking for, which is long income investments with little to no exposure to mid-market fashion, is in very limited supply. This, combined with extended uncertainty around how far rents still have to fall is probably the biggest risk for stunting investment moving forward. This won’t change until investors begin to feel comfortable that the tenant doesn’t have the upper hand in all rent negotiations. Some investors we spoke to at a GRI Club UK and Ireland meeting believed this may happen sooner than people think, despite reports from Savills and JLL not expecting this until much later.

Article by Matt Harris

However, the key drivers shaping retail supply and demand are very different to that seen during the Financial Crisis, with such things as ecommerce and click and collect impacting the industry in ways that weren’t even comprehendable 10 years ago. This unchartered territory has unearthed some quite exciting opportunities: some of the largest transactions across Europe in the last 6 months have seen high-profile acquisitions of non-performing retail parks and shopping centres by companies ready to push them into the 21st century with updated technological and social strategies. With this, and global real estate leaders choosing retail as the second most promising asset in the next 12 months in the latest GRI Chairmen’s Predictions survey, 2020 might actually be the year that the UK and even Europe sees the resurgence of retail.

Investment in UK high street retail shops was fairly strong in 2019. One advisor told the GRI Hub that they estimated around £2bn of retail transactions took place in Q3 2019, compared to £1.8bn for the same period the previous year. Recent reports of large deals being made in London's prime retail locations may be indicative of a rising private investor interest in high streets.

The lack of interest in the shopping centres however has stunted growth, with a lacklustre Q3 2019 only clocking around £650mn in shopping centre deals (Preqin), compared to £974mn in the same period in 2018. However, this is despite super-prime shopping centres yielding 5.5% - the highest it's been since 2017 (Savills). Secondary and Tertiary yields were performing well too (11.25% and 14.5% yield respectively). The Q3 numbers also don’t reflect the growing interest in niche shopping centre assets, such as food anchored real estate.

But what investors are really looking for, which is long income investments with little to no exposure to mid-market fashion, is in very limited supply. This, combined with extended uncertainty around how far rents still have to fall is probably the biggest risk for stunting investment moving forward. This won’t change until investors begin to feel comfortable that the tenant doesn’t have the upper hand in all rent negotiations. Some investors we spoke to at a GRI Club UK and Ireland meeting believed this may happen sooner than people think, despite reports from Savills and JLL not expecting this until much later.

Article by Matt Harris