Credit: Jacksonnick | Envato

Credit: Jacksonnick | Envato Investing in UK real estate impacted by politics and economy

Real estate awaits valuations while market leaders discuss possible Labour government policies and the UK’s investment appeal

The UK’s Economy

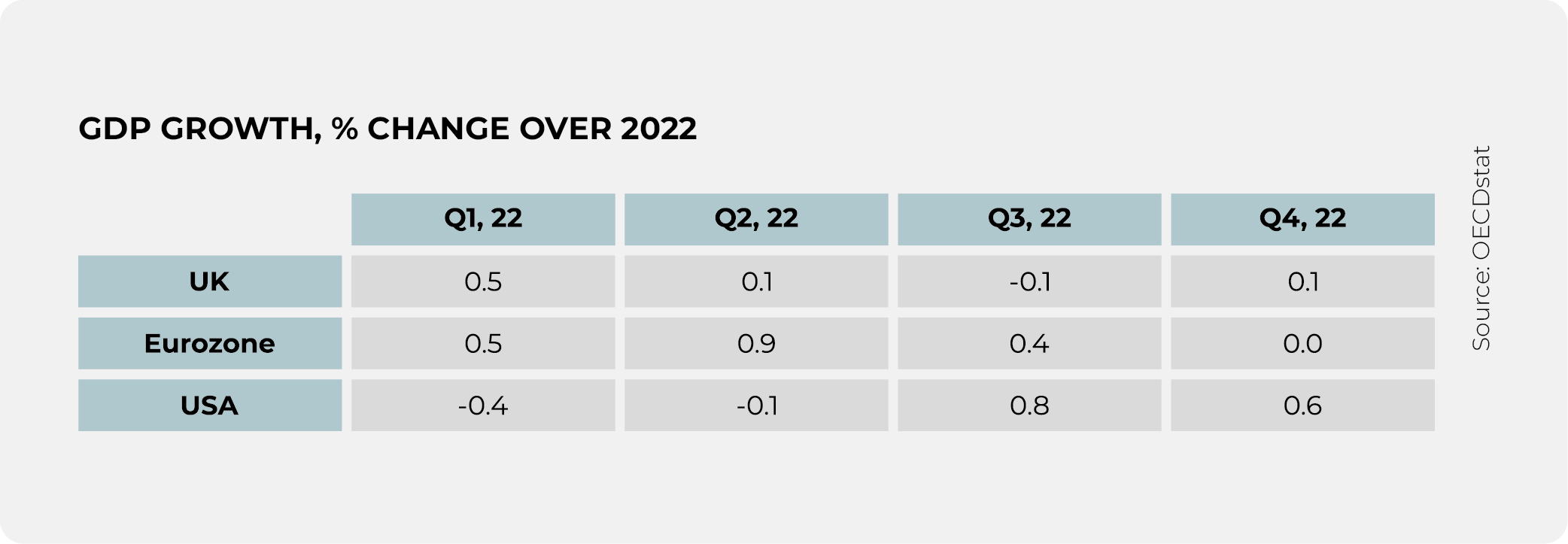

The overall consensus is that the UK’s economy appears brighter than what was predicted at the end of 2022, although productivity and inflation still remain a concern.At the end of 2022, many thought that the UK would be hit by a recession due to the negative growth of Q3. However, there was a small recovery in Q4, hinting at the country’s resilience. Outlooks have changed from the Office for Budget Responsibility, and while there may be negative growth overall this year, it is unlikely that there will be a recession.

The UK's GDP declined by -11.0% in 2020, and the OECD forecasts a 0.2% decline in 2023, which is the lowest figure among the G7 countries. The country’s economy is services driven, and this sector has seen a difficult recovery since the pandemic, but this is in addition to a weak net-trade position and low productivity.

Since the 2008 financial crisis, London's productivity has been down due to its reliance on financial services, which has led to lower numbers than the rest of the UK. Many are still unsure whether these figures were ultimately caused by Brexit.

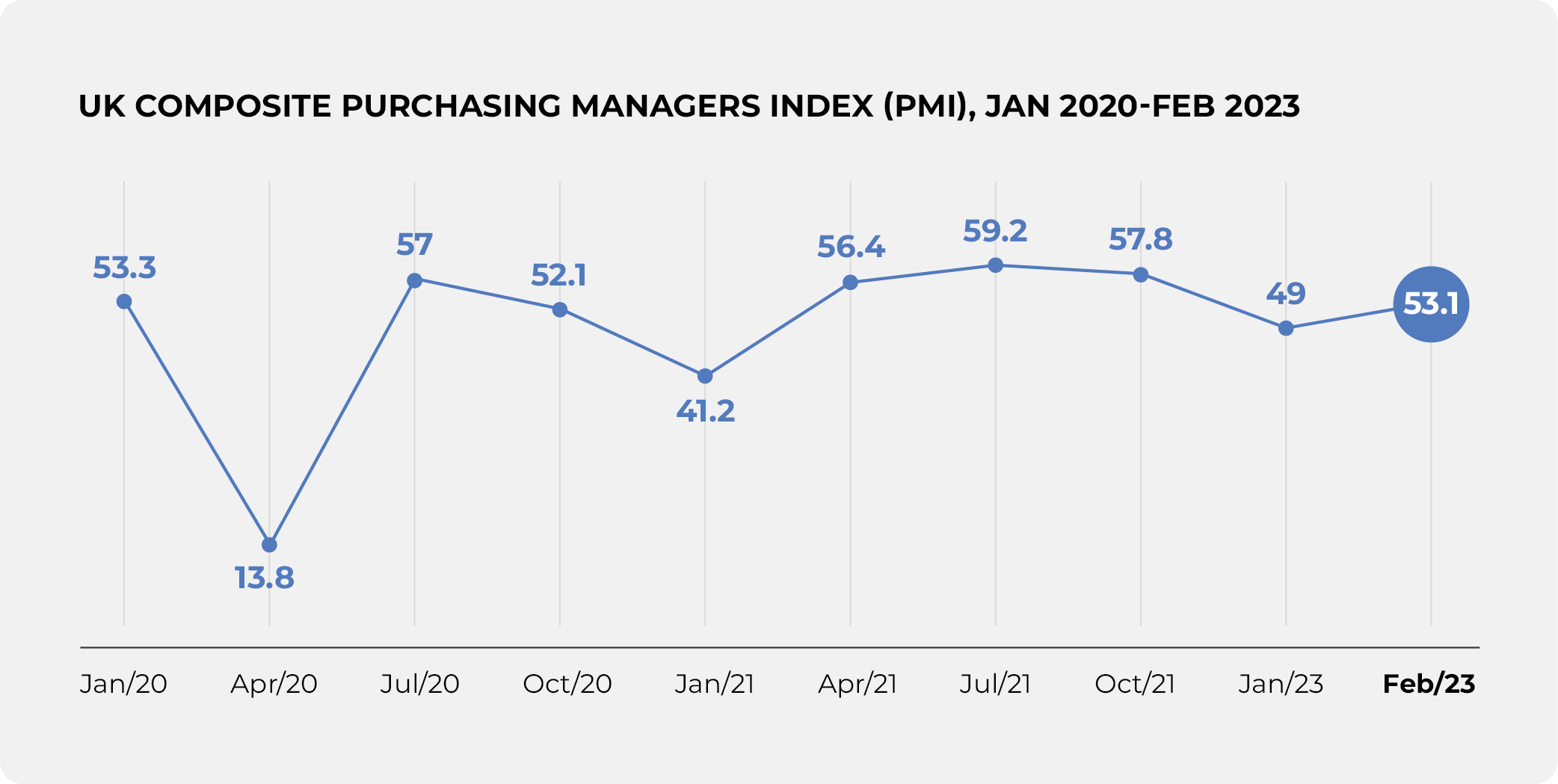

GDP is also monitored by month, and this figure is volatile but in January, the numbers were positive, and February is expected to follow the same trend. The Purchasing Managers Index is also used to understand a significant proportion of the economy, and it appears from these figures that there will be growth, although this depends heavily on the public sector and retail sales - the latter of which have suffered from the ongoing cost-of-living crisis.

Inflation is, of course, always on the minds of real estate players, due to its impact on financing. Inflation has hit hotels and restaurants, clothing and footwear, and food the most significantly. Currently, UK consumer price inflation is 10.4%.

The Bank of England intends to bring this back to the 2% target, and the most recent BoE Monetary Policy Committee meeting saw the bank rate increase to 4.25%. Most GRI Club meeting attendees are in agreement that interest rates will be lower at the end of the year.

For productivity growth, attendees recommend more business investment on behalf of the government, which many feel has always been poor in the UK; many policies put in place have not remained for an adequate length of time.

The Super-deduction Policy implemented during the pandemic was referenced as a positive development by the government.

- The program operated from 1 April 2021 until 31 March 2023.

- Companies investing in qualifying new plant and machinery assets were able to claim a 130% super-deduction capital allowance on qualifying plant and machinery investments.

- There was also a 50% first-year allowance for qualifying special rate assets.

- Q4 business investment numbers were high, but this was a limited program.

The country's economy appears to be stagnant at the moment, but the numbers do not seem overly negative, and there may be growth by the end of the year.

The attending members also touched on the subject of the Silicon Valley Bank crisis and its effect on Europe, but the general sentiments trended positive in this respect. Most European real estate leaders are of the opinion that this is not a full-blown financial crisis and that the central banks have stepped in quickly to prevent any overwhelming ripple effects.

Read more: The impact of the SVB crisis on Europe, from GRI’s recent worldwide online meeting.

The ‘tight’ labour market

The labour market has a significant impact on the economy and was often mentioned at the meeting. The UK employment rate was estimated at 75.6% from October to December 2022, 0.2 percentage points higher than the previous three-month period. The increase in employment over the latest three-month period was driven by part-time workers.During a recent speech at the London School of Economics, Bank of England Governor Andrew Bailey discussed the labour shortage and explained that the UK's ageing population, early retirement of those aged 50-64, and the rise in the number of people who are unable to work are the primary reasons behind this reduction in labour supply. Last year, he was one of many who referred to the labour market as ‘tight’, with more jobs available than workers to fill them.

Some at the meeting emphasised that it is not just higher productivity that is needed for the UK economy, but also more skilled workers, who may have been prevented from entering the UK by government restrictions on immigration.

As there is a labour shortage, many would expect businesses to invest and create a digital revolution. However, this digital revolution has not yet happened to a significant extent; although, some GRI members are of the opinion that it may in the next five years.

Valuations

At the moment, many are still waiting for valuations to kickstart the UK real estate market, which appear to be delayed due to the environment of high inflation and past months of uncertainty. The release of valuations is predicted to trigger deals and transaction volume to increase.

This was also emphasised heavily in GRI Club’s first main event of the year, the GRI UK & Europe Club Reunion. Read the report from this event, featuring valuations and asset class discussions.

There is now a large funding gap for commercial real estate, and there are several options for leveraging, one of which is mezzanine funds, which look to some to be ‘really exciting’ as an alternative to equity. But, this is on the basis of interest rates being reduced quickly. These are bridging loans to get back to a more normalized senior debt market. From a funds perspective, many are seeing special situations starting to be interesting, as well as recapitalization funds to come into these structures and take that gap.

Government policy

GRI Club members showed concern over the wavering government policy for housing as well as the uncertainty over Conservative Party intentions. Many agreed that they were unsure where the government hoped to put capital investment, which has a multiplier effect and is therefore vital. Last year’s mini-budget, prompted by Liz Truss, frightened markets as its funding methods were unclear.

UK housing is backed by ‘unbelievable’ demand, and low supply - an issue that worsens year on year, and also plagues much of Europe. There are 1.2 million households on the social housing waiting list. It is important that, due to the nature of government changes and its 5-year cycle, there is cross-party consensus on how to achieve goals such as increasing the supply of housing.

Read: on the new housing policy in Portugal, which faces some of the highest rents on the continent.

There are approximately 50,000 affordable homes built a year, but these numbers need to be tripled. The planning system is often blamed in the UK for this supply-demand imbalance, and it is certainly a contributing factor, but affordable housing deliveries are funded in a way that means that high targets cannot be met.

Chalabala | Envato

Chalabala | Envato

The Conservative Party’s housing policy is complex and controversial within the party itself. In its 2019 manifesto, the Conservatives promised to build 300,000 new homes a year. This led to a relaxation of the planning system that was heavily debated. Also, attendees asserted that one issue with home development is that taxes and regulations account for a quarter of expenses when building even large numbers of homes, with planning delays creating cost barriers.

Proposals from the club meeting for ways the government could improve the existing landscape include:

- Reducing financing costs, which are an issue for many student housing investors and funds, as well as the whole bed sector, hurting investment positions due to a lack of rental growth and profit margins.

- Decreasing the corporate tax rate, which is not comparable globally. Many investors will choose other regions to invest in that have a lower tax rate, such as the USA.

- Increasing communication and coordination between different government departments, as the housing ministry needs more communication from departments such as the treasury on issues such as corporation tax.

Predictions for a possible Labour government

UK polls suggest that the Labour Party may in fact form the next government at the next election, and the meeting attendees discussed the potential policies they may implement. Firstly, many assume that they will invest further in green technology and encourage ESG investment.

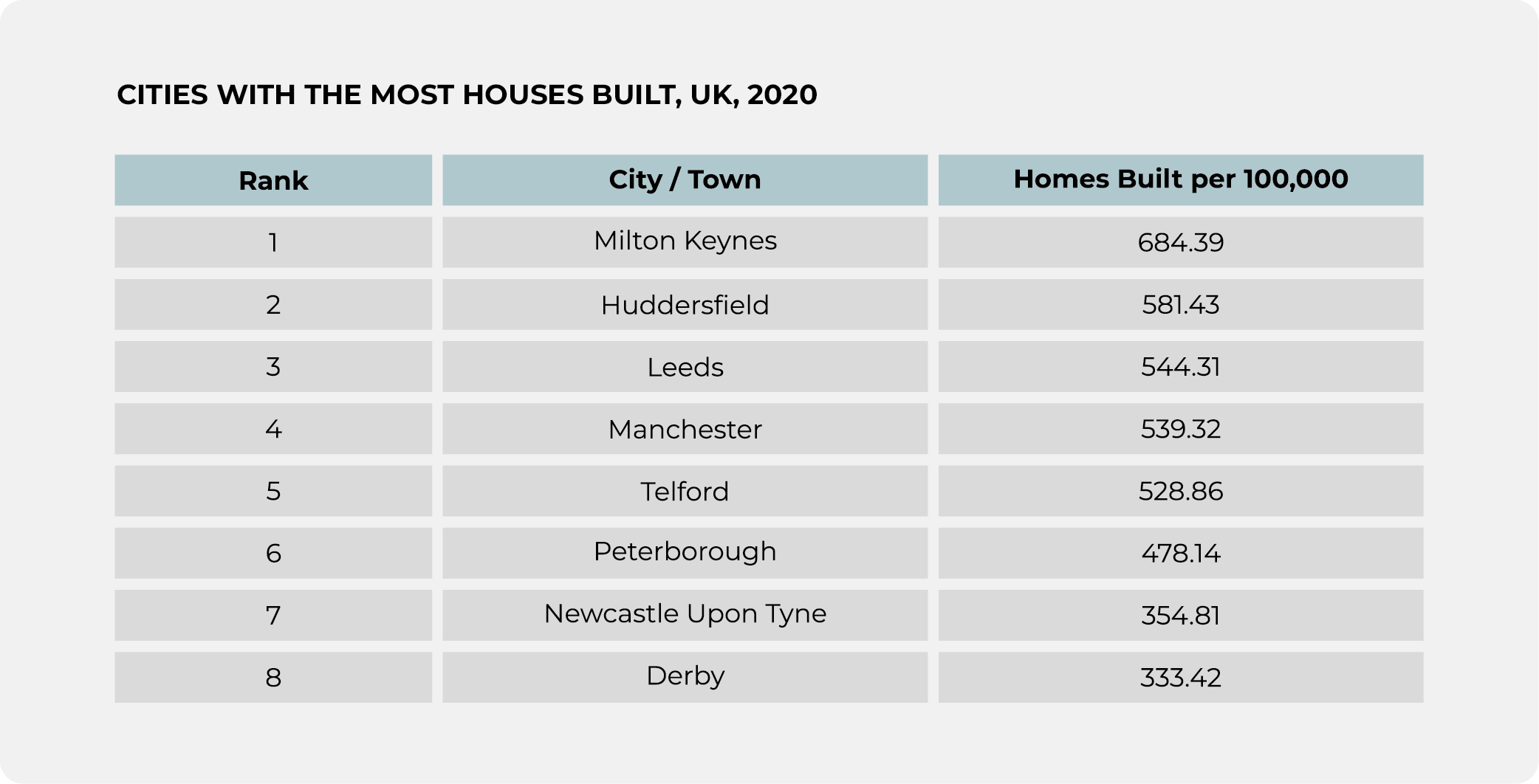

Many attendees expect an increase in house building under a Labour government, while it is likely that building regulations will also increase. This is because Labour will be free of the politics of small home counties that the Conservatives suffer from. Currently, the south and midlands of the UK receive fewer new homes; in 2020, the cities with the least number of homes built were Leicester, Blackpool, Portsmouth, London and Luton.

There are mixed views on whether Labour would implement rent controls if in power. An alternative would be that they encourage fair tribunals where tenants can submit complaints about the price of rent. Many feel strongly about the negative impacts of rent controls, as construction costs continue to rise while rents remain the same. Caps such as these are a considerable risk for investors, and clarity of discussion and working with investors who understand the risk of potential political intervention is key.

Decarbonisation

One of the main concerns as well as challenges for those developing in all asset classes is the effective decarbonization of UK buildings, as well as the need to make existing portfolios more sustainable as well as fire safe.

Many predict that developers will be told to prioritize decarbonization as well as safety above all, and as a result, new home development will be pushed back. This will occur in a cost-of-living crisis where developers, as well as UK citizens seeking affordable housing, cannot afford it.

Skilled labour shortages and low productivity in the UK could be a multiplier effect for obtaining government expenditures, particularly considering the decarbonization agenda. Thousands of homes need retrofitting, and skilled labourers are needed, for instance, to install air source heat pumps or insulate older homes. General government intervention could be positive in this area.

The UK’s attractiveness to investors

How has the relative attractiveness of UK real estate been affected by politics and the economy?

- Many are concerned about the weakening of the GBP compared to Ultimate Secure Cash (USC).

- Investors are uncomfortable without a stronger economic recovery.

- Political factors that have weakened the UK in investors' eyes are Brexit, Liz Truss’ budget, and the fact that the country has had 4 different prime ministers since 2019.

However, those still interested in the UK will look at London first, and the drop in valuations will make it more appealing to investors, as well as the fact that the UK has the ability to recover quickly.

Attend Europe GRI 2023 to discuss investors’ views on UK and European real estate, as well as to meet the most relevant market leaders.

Written by Sarah Garnett