ABBPhoto | Envato

ABBPhoto | EnvatoA Guide to the Hotel Outlook for Spain, Italy and Portugal in 2023

The end of 2022 confirmed that the European hotel market had ended the year on a high, with Revenue Per Available Room up 13% compared to 2019, driven by higher prices on average. Occupancy rates also increased, returning to only slightly below pre-pandemic levels. Spain was one of the countries that led this success.

Leisure Hotels also made the top 10 for rent sector prospects in the Emerging Trends in Real Estate survey from PwC this year. Business Hotels, on the other hand, fell to the bottom of the list. Leisure travel saw a boom after the effects of COVID-19 softened, with younger age groups and middle classes focused on new experiences, although some may still be hesitant to invest due to cost-of-living crises and interest rate hikes across Europe.

Read: on the ‘hotelisation’ of real estate

-

Data has been key in transforming the real estate industry, with the transparency it provides helping investors to understand the differences between sectors.

-

Trends that are ongoing or emerged from the pandemic include queueless receptions, sustainable hotels, strengthening client loyalty, remote working, and longer hotel stays, which has introduced new opportunities for growth and profit.

Southern Europe has been a leading tourist destination for several years, and Italy, Spain and Portugal’s activity almost reached pre-COVID rates in 2022. 2023 is set to be a year of growth and profit.

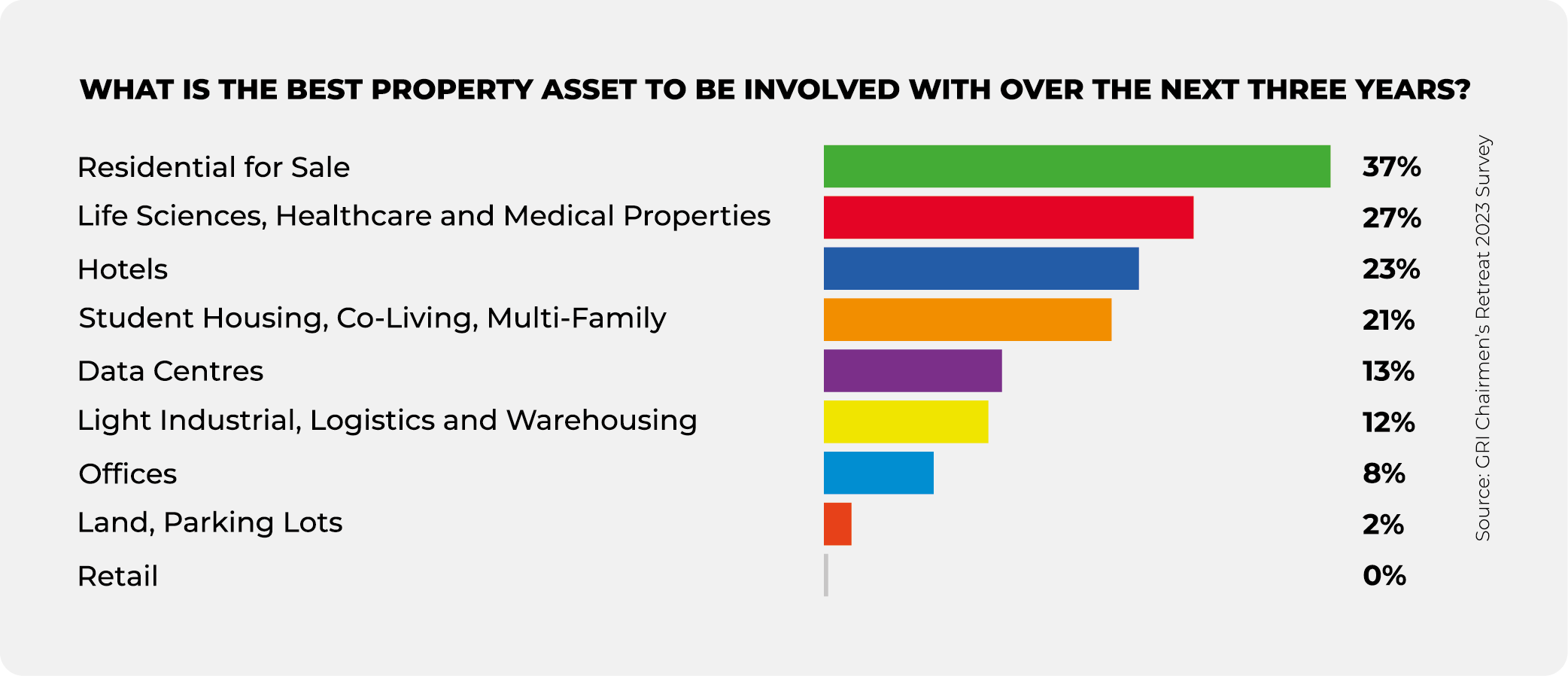

In terms of investor choices and strategy for Hotel investments, factors such as return requirement and risk appetite are major drivers. Spain, Italy and Portugal are frontrunners for resorts in particular with Spain in the lead, according to Christian Kaufmann, Director of the Hotel Investment Properties team at CBRE.

Spain leads hotel investments and developments

CBRE’s Investor Intentions Survey 2023 shows that Spain is one of the best countries to invest in this year, behind only the UK, Germany and France, and it was Hotels and Logistics that had the highest rates of profitability in 2022. The hotel sector generated returns of more than 4.75%. Both Madrid and Barcelona were listed among the top 10 European cities to invest in, coming in fifth and sixth place respectively.

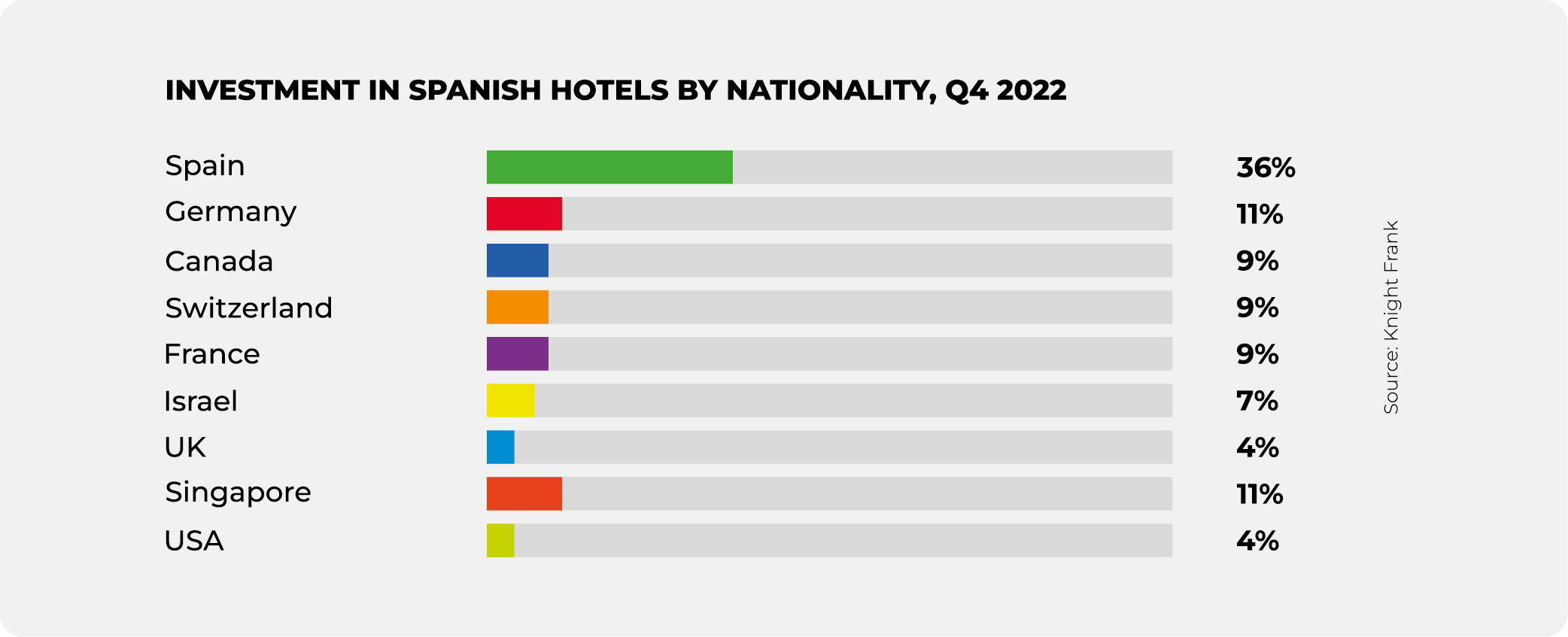

Spain’s success began pre-pandemic, and Hotel investment reached over €2,100 million by the end of 2021, an improvement on the figure recorded for 2020 with Madrid and Barcelona the hottest investment targets. Spain then welcomed more than 71 million international tourists in 2022, spending on average more money and time in the country than before the pandemic.

This year, inflation is predicted to be less dramatic than Europe’s average, dropping from 8.7% to 3.7% in 2023, which is a good sign for real estate investors and lenders.

Meliá, the largest hotel operator in Spain, is an example of this success.

-

The group reported a net profit of 120.1 million euros ($127.40 million) compared to a net loss of 192.9 million euros one year ago.

-

2022’s profit was only 1.3% below 2019, but well ahead of analysts’ estimates for a 58 million euro net profit, according to Refinitiv.

-

Half of this 2022 profit came from Spain.

-

Meliá has leaned into luxury with its latest brands, such as the Gran Meliá, the ME, and the Meliá Collection.

-

Meliá supports the regeneration of destinations in collaboration with locals, as refreshing ageing infrastructure and amenities, such as upgrading roads, improving taxi service, and doing upkeep on beaches, is incredibly beneficial for business.

-

Read: Melia Looks for Partners to Grow Premium Resort Portfolio

Source: SeanPavone, Envato

Source: SeanPavone, Envato

New Spanish hotel developments:

-

Hilton to debut in Spain’s Extremadura region with 16th-century palace property, Palacio de Godoy Cáceres.

-

Redevco enters the hotel sector with €80m foray into the Iberian market. Read more here.

Spanish hotel investment locations

The population of Spain’s Balearic Islands has increased 50% since 1996, mainly due to a surge in newcomers attracted by the beaches and sunny weather. The trend gathered pace over the past few years as the Covid pandemic increased the number of remote workers on the islands.

This has created a problem with a lack of housing product and soaring prices, with rents increasing 15% on the islands year-on-year, and locals left behind with these cost-of-living increases. Seasonal demand for staff for hotels and other tourist amenities has only worsened the issue; Ibiza and Mallorca have been shifting their focus to luxury tourism in order to distance themselves from the image of "party islands." Ibiza has doubled the number of high-end resorts since 2016, while ten new five-star hotels were built in Mallorca in the last 5 years.

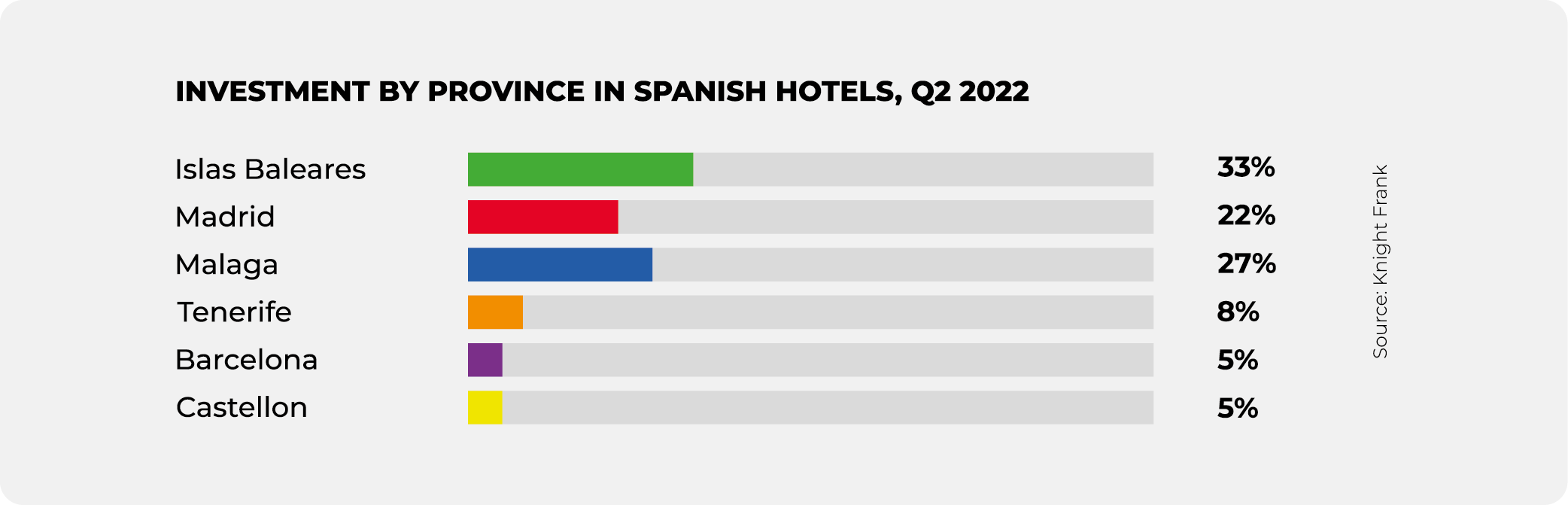

Meanwhile, Barcelona has seen a moratorium on hotel projects since 2015, with a huge number of projects put on hold since then. This helps to explain the lack of investment in the province.

Madrid has instead become a leading location, and investors dedicated a total of 803 million euros to the acquisition of hotels in Madrid during 2022, which represents an increase of 72% compared to the previous year.

Portugal’s hotel operation indicators

Source: diego_cervo | Envato

Lisbon was also mentioned in CBRE’s top 10 European cities for investments, and while Portugal may not rival Spain in investment volumes, it demonstrates its own success; according to Cushman & Wakefield, Hospitality in Portugal is a “dynamic sector”, and contributed 30% to the country’s total real estate investments in 2022.

Portugal follows the Southern European trend of bouncing back post-COVID, and around 115 new hotel projects are in the design and/or construction phase, totalling 9,900 rooms, with openings scheduled for the next three years.

Between January and October, the number of guests and overnight stays registered a year-on-year increase of 98% and 100%, respectively, just 2% below the figures for 2019.

-

As a result of the growth in demand, hotel operation indicators reflected significant increases in total income at a national level, 130% above the same period of the previous year and also 14% above 2019.

-

Last year, tourism performance spurred investment initiatives including sale & lease-back operations and platform acquisitions.

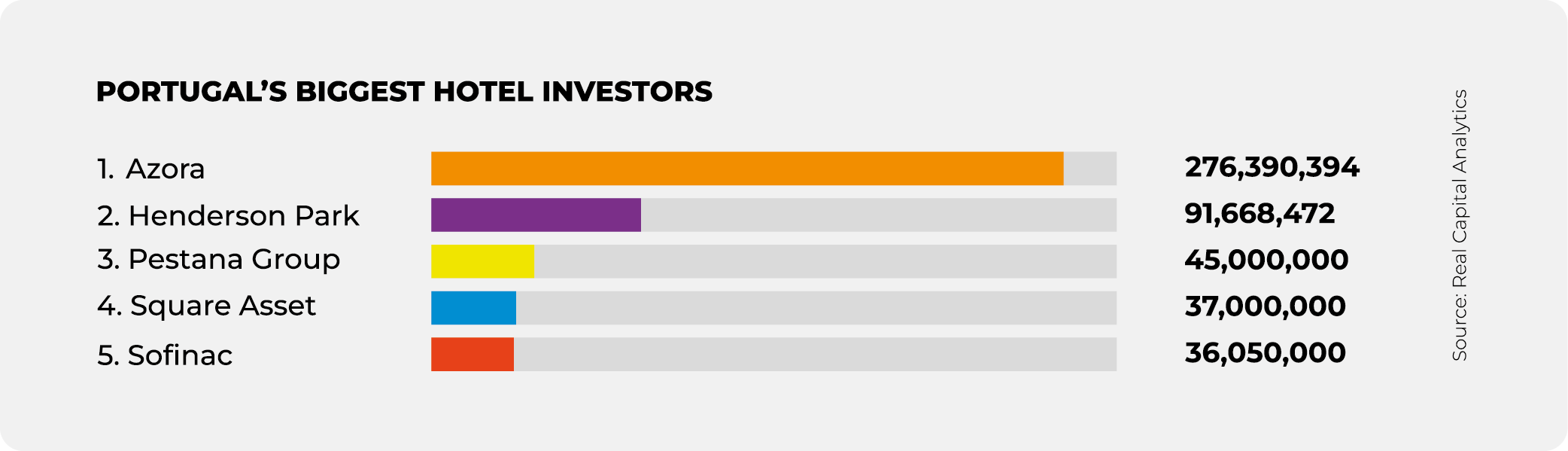

In the list of hotel investments and transactions for 2022, highlights include the acquisition of Pestana Blue Alvor by Azora, for 80 million euros, and the sale of The Lodge Hotel to Azora Capital for 50 million euros. Spain and the USA lead the way in terms of international investments.

Hospitality investors await valuations and clarity for 2023

“After a surprisingly positive year for the Portuguese market, considering the circumstances, we are a little more cautious with regard to 2023. Portugal will not be immune to the climate of apprehension that reigns in northern Europe, where, in fact, many of the decisions regarding investment in our country are taken,” says Eric van Leuven, managing director of Cushman & Wakefield in Portugal.

As interest rates rise, the real value of assets becomes uncertain, which will cause investment decisions to be delayed until more clarity is provided. However, Portugal appears to still be very much in the eye line of investors and developers.

Recent Portuguese Hotel news:

-

In January, investment manager Davidson Kempner closed a deal purchasing 850 euros of hotels, including the Palacio do Governador, the Conrad Algarve, and the Hilton Vilamoura As Cascatas Golf Resort & Spa.

-

In February, Socicorreia invested €100m in residential developments and hotels, including the construction of a 5-star hotel in Braga.

In recent weeks, Portugal’s government also began to implement measures against Airbnb and short-term rentals in their ‘Mais Habilitacao’ program, which for many tourists were the immediate alternative to hotels. This posits an interesting opportunity for the Hotel sector, particularly for hotels that offer home-like amenities at affordable prices. The rules prevent emissions of new local housing permits, with the exception of rural housing where they can boost the local economy.

The new program has been criticised by real estate players for the end of the golden visa, as well as by associations such as the Association of Hotels and Tourist Developments of the Algarve (AHETA). The Association has stated, "The rules adopted in the last Council of Ministers are killers of local accommodation and who will announce their death, in a very short period."

Read more about the end of the Portuguese golden visa and the real estate industry’s opinion.

Italy: from economy to luxury hotels, a fractured market

The potential of Hospitality as an asset class in Italy was discussed at GRI’s club meeting this year. Italian market experts noted that the market is fractured, which in itself opens opportunities for interesting deals with independent owner families.

Despite this, hotel chains are still finding success in Italy; one out of every five hotel rooms is owned or managed by a chain. However, it is likely that the boom in acquisitions made pre-Covid will not be repeated, due to a complex economic and geopolitical situation that leads to caution.

You can read more about the market in Italy from GRI’s investors and developers involved in the market here.

![]()

-

Hotel asset management: Lvmh takes over 2 hotels on the Costa Smeralda.

-

Hotel development: Marina Development Corporation develops 60 million Euro project in Ventimiglia, and ECE division undertakes their first hotel development in Italy.

Luxury hotels have been highlighted by GRI members as an opportunity, with many tourists from the US choosing Italy for travel and having large amounts of capital to spend. Due to numerous repositioning and conversion operations, Rome represents the most dynamic market in terms of its luxury hotel offer today. The Italian capital's hotel offer is estimated to boast the opening of over 2,000 new rooms within the next three years, mainly in the lifestyle and luxury sectors.

-

The Six Senses Rome, which opens this month near Via del Corso, is the brand's first urban property.

-

In February, there were investments of 500 million for luxury hotels in Florence, from Marriott, Auberge Resorts, Gb Invest, and Baccarat Hotels & Resorts.

There is also a contrast between ‘top-luxury’ and ‘non-top-luxury’ hotels, with the former having a less significant drop in revenue during the pandemic (-53% vs -71%), and better recovery, with turnover only 10% lower than 2019’s numbers. However, it is the non-top-luxury hotels that recorded higher Earnings Before Interest, Taxes, Depreciation and Amortisation (EBITDA) from 2018 to 2021.

For the economy segment, according to a recent analysis by Thrends on Italy over the last decade, accommodation facilities saw a decrease equal to a Compound Annual Growth Rate of -2.8%. However, the leading chains saw a growth of 23.9%.

In 2022, 60% of the affordable-targeted properties were owned compared to 40% that were leased, with ownership constituting the most prevalent business model.

-

Bella Italia holds the record in the segment with 794 keys. The presence of the chain in the segment is mainly concentrated in Northern Italy.

-

The presence of hotels in the economy segment is destined to increase in the coming years, which will see the opening of 6 chain structures, mostly concentrated in central Italy.

-

On Italian soil, the number of chains in the hostel segment is particularly limited and rather stable.

-

Operators offering flexible stay formulas are growing, such as Camplus, CXPlace, Staycity, The Student Hotel and, in the scouting phase on Italian soil, Selina and Edyn.

Southern Europe is predicted to have a positive 2023 for Hotels, while investors and lenders now understand that what was a previously ‘alternative’ asset class is, in fact, a significant and more importantly stable opportunity.

To discuss hospitality in Italy, Spain, and Portugal, secure your place at their respective GRI events in the coming months. The first event is GRI España 2023 in Madrid on April 24-25.

Written by Sarah Garnett